Welcome to the ultimate guide to 2019 and 2020 Self Employment tax! This all encompassing guide will take you from zero knowledge to beginning your own Self Employment tax strategy.

Along the way you’ll learn what it is, why it matters, who pays, and most importantly how to avoid it.

What is Self Employment Tax?

Refers to the combination of Social Security and Medicare taxes imposed on people that work for themselves.

Contents

Chapter 1What, Who, Why

What exactly is this tax, who pays it, and why does it matter? In this chapter you’ll learn about what makes up this hefty tax and if it applies to you. Lastly, we’ll learn why understanding this tax will have a dramatic impact on your financial success as an entrepreneur.

What is The Self Employment Tax?

Self Employment (SE) Tax is a major tax defined by the “Self Employed Contributions Act (SECA)” of 1954. It’s purpose is to fund Social Security (SS) and Medicare from the net income of self employed people. Employees and employers pay a similar tax called FICA, which is why tax professionals often refer to Social Security and Medicare taxes “FICA”.

Now whether you’re an employee or working for yourself there’s two “portions” of this tax: employer and employee. If you’re self employed the IRS considers you both the employer and employee. That means you are responsible for both portions, while employees are technically only held responsible for theirs.

Who Pays and Who Doesn’t?

At around 15.3% (we’ll get into that next chapter) of your net income, SE Tax isn’t chump change. So who has to pay?

You pay if you’ve earned more than $400 from self employment income and you’re a:

Sole Proprietor (AKA freelancer, independent contractor, 1099-Misc)

Partnership

Single-Member LLC (by default IRS treats you like a sole proprietor)

Multi-Member LLC (by default IRS treats you like a partnership)

… and you make Ordinary Income through sales of a product/service, commissions, short term capital gains, and even flipping houses.

You don't pay if you did not earn more than $400 from self employment income or you’ve:

Opted for a S-Corp tax classification

Opted for a C-Corp tax classification

And/or your income came from IRS preferred activities: rental income, long term capital gains, qualified dividends, and some kinds of interest.

Heads Up

In some of these you’re paying into FICA instead of SECA. So you’re still paying Social Security and Medicare, however we’ll discuss why you may want to do that in Chapter 4.

Why Does Self Employment Tax Matter?

Let’s not beat around the bush: if most of your income is from working for yourself, then Self Employment tax is likely the biggest single tax you have. Since your greatest expense is taxes, having a plan for dealing with this tax is critical! Secondly, unlike employees, you’re held 100% responsible for paying this tax yourself. Simply put: unless you take action, your self employment income will be subject to some very costly taxes. That’s the bad news.

Good news is that running a business opens up a world of possibility to avoiding SE tax, which we’ll talk about in Chapters 5 & 6. First we need to figure out how big of a tax burden you owe.

Chapter 2Calculating Your Taxes

In this chapter we talk about brass tax (apologies if you’re manufacturing brass). Calculating SE tax isn’t as straightforward as multiplying your net income by 15.3%. We’ll walk you through automated tools, relevant IRS forms, calculating by hand, and some tips to keep you from getting blind sided by SE Tax. Let’s get started!

Not Your Final Tax

Calculating your SE Tax is a critical step to improving your tax strategy, however it’s by no means your final tax! To get a better picture of your final tax obligation you’ll need to account for income taxes, both federal and/or state.

Recommended: Use Our Calculator

Checkout our automated Self Employment Tax Calculator. Just input your information and it does the legwork for you. However if you’d rather crunch the numbers yourself please read on.

Manually: Calculate by Hand

First calculate your business net income, you want this number as low as possible for tax purposes. Next we find the employer portion of SE to deduct: Net Income * 7.65% (6.2% for SS and 1.45% for Medicare). Subtract that employer portion from your Net Income and multiply it by 15.3% to get your SE Tax. A simpler way to get the same result is: Net Income * 14.13%. Here’s it all written out:

+ Business Net Income

- SE Tax Employer Portion Deduction x 15.3% = Your SE Tax

*Note this is just an estimate, which is not considering a lot of factors (especially for high income earners).

Real World Example

Let’s say Janet earned a tidy net income from her business of $100,000. Let’s estimate what she owes in SE Tax.

+ 100,000 Business Net Income

- 7,650 Employer Portion of SE Deduction

X 15.3%

$14,130 Self Employment Tax Owed

Or use the quick way 100,000 * 0.1413 = $14,130. Now let’s take a look at a high income earner, which has more factors to consider.

Extra Considerations For Higher Incomes

Two things to consider if business is booming: Social Security’s cap and Medicare’s extra tax. For 2019 Social Security only applies to your first $132,900 of combined income ($137,700 in 2020), so if you pass that it’s good news! Bad news is Medicare is uncapped and even adds on another 0.9% tax to all income over $200,000 (single filter) or $250,000 (married). If your head’s swimming please checkout our calculator, which will does all this heavy lifting for you.

It's Not Over

As we conclude this chapter it's important to be aware of where we are in the journey of your income from your business into your pocket. Previously we mentioned your self employment income is double taxed, because it's important to understand why.

Self Employment Tax is only the first major round of taxes your business income is subjected to. Next up will be Income Taxes, where your income meets its’ second round of taxes. Income and State Taxes are outside the scope of this guide, however at least now you’re aware you’re in the first half of the game.

Chapter 3How To Pay Self Employment Taxes

Now that we’ve covered why the SE Tax is worthy of your attention, our next concern is how can you pay it while minimizing stress. Key questions are: “should I pay quarterly or annually?” and “how should I budget for it?”. We’ll tackle both of those questions as well as how to plan head and avoid tax stress before it snowballs out of control.

Note: I’m assuming you’ve earned at least $400 in net income for the year in question, otherwise you don’t owe any SE Tax. However you're still required to file a 1040.

Paying Quarterly vs Annually

Unless a CPA or Accountant told you not to: you’ll be paying SE Tax quarterly as a part of your estimated tax payments. All self employed people expecting to owe at least $1000 in tax (not just SE Tax) for the year should probably be making quarterly payments, so if you’re unsure go with quarterly payment. IRS provides all the information you need to calculate and make these payments in this big 2019 Form 1040-ES PDF.

Here are some important cliff notes before you dive into Form 1040-ES:

1040-ES payments must include estimates of your federal income taxes in addition to your SE taxes.

These payments are self reported - while required for most self employed people, they are essentially a best guess of the taxes you’ll ultimately be responsible for. Your final tax obligation is decided on your 1040.

Overpayments of these estimates can be returned to you or applied as future tax credits.

It’s better to overestimate payments to avoid extra paperwork and expensive penalties.

Avoid The Penalty

Obviously you want to avoid the late payment of Estimated Tax penalty, with its’ costs ranging from mild to painful. It’s not uncommon for the newly self employed to have to pay penalties after learning they should have been making estimated payments. If this describes you then don’t beat yourself up, many entrepreneurs have made this same mistake! Here’s 2 popular approaches to estimating what you may owe:

Optimistic: 4% x (Amount you owe) x (days late / 365). Example: 0.04 x $1000 x 30/365 ≈ $3.29

Pessimistic: 3.603% x (Amount you owe). Example: 0.03603 x $1000 = 36.03 (assumes your payment is exactly 1 year late).

Again these are just popular ways to ballpark the penalties. Keep in mind the penalty can be as much as 25% of the cost of your total taxes, so act quick if you know you're behind! Ultimately you'll be using IRS Form 2210 to calculate the exact penalty amounts and add the result to your 1040.

When It’s Your First Year In Business

When you read Form 1040-ES that a lot of Estimated Tax payments is based on your prior year’s income. If you think you’ll owe taxes over $1000 you still need to make quarterly payments, you’ll simply be doing more guess work throughout the year. Use 2019 Form 1040-ES as well as your most recent expected income (from most recent quarter) to calculate your estimated payment. Your payments don’t have to be the same every quarter, we are just looking to get at least 90% of your actual tax obligation estimated. That way you won’t own any penalties!

When You’re Making Less than Last Year

You’re still expected to pay the prior years estimated payments. Yes you read that right: even though you’re making less than you did last year you still have to make excessive estimated payments. That said you still have options you can consider outlined in this post.

How to Pay Estimated Taxes

All payment options are listed in detail towards the end of Form 1040-ES however the most popular options are IRS Direct Pay and mailing in a check with your voucher. You’ll find those 1040-ES payment vouchers at the very end of that PDF download, which you’ll need to fill out for the relevant quarter and send it in with your check. Last but not least, quarterly payments should be made before:

Q1 - April 15th

Q2 - June 15th

Q3 - September 15th

Q4 - January 15th of the following year

Planning for Self Employment Tax

Setting aside some of your revenue for the pain of Self Employment tax is crucial to preventing stress and keeping your business out of crisis. Financial planners use a 30% rule of thumb, which means that for every dollar of gross profit you set aside 30 cents for taxes. The 30% rule of thumb could be too much or too little depending on your situation, so please do your own research. However much you set aside, having a bank that’s able to support you makes this process far easier.

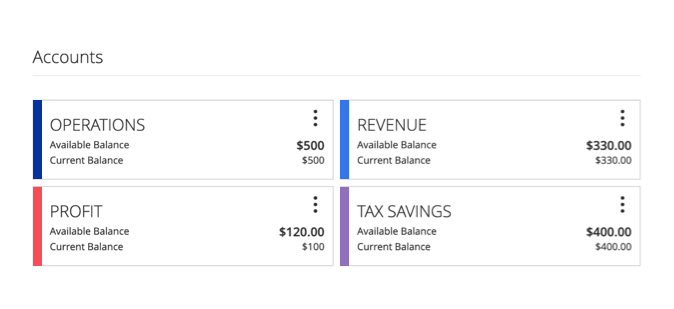

Use Bank Accounts to Keep You Organized

Here’s an example dashboard of using separate checking accounts to run your business. You can’t get this level of organization with a single business account! Please make note of the last account named “Tax Savings”. This is the secret sauce to keeping your taxes budgeted for throughout the year.

Join a bank that will allow you to set up multiple business accounts, specifically one for taxes. This is the simplest and most effective way to budget for these SE Taxes. If your bank gives you any grief about setting this up, then you should absolutely find a new bank. I’ve found Credit Unions to be far more accommodating than big banks like Wells Fargo, however it’s best to ask around. There’s plenty of other helpful accounts you can setup outlined in the book Profit First by Mike Michalowicz however here’s his free resource about setting this up for yourself.

Now if you’re asking yourself: “30 cents of every dollar? Is he serious?!”, you’ve got the right idea! Paying 30% or more of your net income to taxes is a strong sign you need a better tax strategy, let’s discuss common tax strategies for self employed people next.

Chapter 4Avoiding Self Employment Taxes

If you’re new to being self employed, avoiding the crushing SE taxes is often your largest source of tax savings. Please note I’m using the word “avoid” here because we are not interested in “evading” taxes, which is illegal. Avoiding taxes is completely legal and here’s the kicker: the government actually wants you to avoid taxes! Next we create a mental map of how you can start planning your own tax strategy.

Social Security Benefits

As we’ve discussed, SE Tax includes Social Security. Unsurprisingly if you avoid paying Social Security, your payout may be reduced in your retirement. Many people are skeptical if Social Security will exist in its’ current form by the time they retire, but either way know that your benefits may be lower.

Tactics

If timing is a factor your options (as well as tax savings) are much more limited, however there’s still hope! What you can do in the short run to reduce Self Employment Taxes is to maximize all possible deductions and minimize penalties as discussed in Chapter 3. While deductions are a critical part of every tax strategy, ultimately the biggest savings will come from improving your strategy. We’ll discuss our favorite deductions and in depth resources in Chapter 5.

Strategy

Any seasoned business owner will tell you having a solid tax strategy is essential to building long term wealth. If you’ve grown a business and are paying more than 30% of your income to taxes the burden can become demotivating and stress inducing. Luckily with a little planning and the right accountant you can take steps to manage SE taxes in a better way.

In Chapter 6 we’ll discuss high level strategies that will have the biggest impact on your financial success.

Chapter 5Tax Tactics: Deductions

Deductions are the low level part of your tax strategy, however they still play an important role reducing your SE Taxes. Before we dive in a word of warning: deductions are a complicated topic! To make matters worse the internet is littered with out of date and low quality information about deductions. While deductions are worth understanding, if you’re new to deductions just focus on getting the most bang for your buck.

Keep It Super Simple

Here’s a simple definition of a deduction: something that reduces your taxes. Good luck getting a definition like that from the IRS! As a business owner deductions are a great advantage you have over employees. However to claim them you often need to do some leg work: planning, documenting, and bookkeeping. So would hiring a bookkeeper set you up to start saving money? Absolutely.

Above The Line

To reduce Self Employment Tax you’ll need to focus your efforts on “Above The Line” Deductions. “The Line” is also called Adjusted Gross Income (AGI), in case you were curious.

Best Self Employed Deductions

There are many deductions, however these are some CPA’s recommend self employed people look into. They can get complicated so discuss each one with an Accountant and come up with a game plan to claim each one:

Qualified Business Income (QBI) - Up to 20% of qualified business income. Huge!

Technology and Equipment - Only % you use for business.

Phone and Internet - Only % you use for business.

Travel Expenses - Takes planning, requires documentation.

Dining & Entertainment - Often only 50%.

Home office - Takes planning (and potentially moving) but saving can be significant

Vehicle - New and improved via the 2017 TCJA legislation

Deduction Resources

The Tax & Legal Playbook (chapters 9 & 10) by Mark J. Kohler CPA, Attorney

Taxpayer's Comprehensive Guide to LLCs and S Corps (chapter 11) by Jason Watson CPA

Chapter 6Tax Strategy

A favorite topic of successful business owners and where great accountants truly shine: tax strategy. Strategies can vary in terms of the impact on your business, so if you’re looking for the biggest savings possible be prepared for big changes. However let’s discuss one popular strategy that doesn’t require dramatic changes to your business.

Become an S-Corp: Small Change, Big Savings

If you have an LLC then opting into an S-Corporation tax classification could massively limit your exposure to Social Security and Medicare taxes. You’ll still be an LLC, however you will become a W-2 employee taking a regular salary. This salary will be taxed at the same rate as your current self employment income, however now you’ll be able to make distributions! These distributions are not subject to Social Security and Medicare taxes so the savings can be massive.

If you’d like to find out how much you could be saving with this strategy checkout our free calculator. It compares your current income against a tax advantaged S-Corp to see if this strategy is something you should consider.

Please consider the tradeoffs you’re making as well: running payroll, exposure to new smaller taxes, calculating reasonable compensation, and more compliance to worry about. Any decent CPA will guide and help you with all of this, just be sure you ask about your role in the quarterly maintenance of an S-Corp.

Other Strategies

Using an S-Corporation is a popular strategy because it doesn’t require big changes to your business, however there’s other options you could consider. In this guide we’ve been discussing Ordinary Income, which gets hit with the most taxes including Social Security and Medicare. There’s other kinds of income that the tax code gives preferential treatment to and avoids SE taxes.

Preferential Income:

Rental Property Income

Long term capital gains

Qualified Dividends

Interest from municipal bonds

And more

Aside from changing your business to get these preferred types of income, retirement accounts can also be a great way to avoid or defer paying SE Tax. Popular options for self employed people to research are: Simplified Employee Pension (SEP) and Health Savings Accounts. This is another complicated topic and outside the scope of this guide.

Chapter 7Conclusion

We’ve covered a ton of ground in this guide, here’s some major take away points about Self Employment:

SE Taxes are effectively a 14.13% tax on the net income of your business.

Higher incomes make calculating SE Tax more difficult, so use our calculator.

Why you’re responsible for both the employer and employee portions of Social Security and Medicare taxes.

How your business net income is doubled taxed: once by SE then again by income taxes.

Why you should be paying for this tax with estimated quarterly payments.

How to set up special checking accounts to help you set aside money for this tax.

How to research and use deductions to limit your exposure to SE Taxes.

How a better tax strategy could likely save you a ton on SE Taxes as well as how to calculate if that strategy could save you money.

If this guide has stressed you out about at all the things you should have been doing, remember a lot of us have been there. Many Self Employed people have found themselves blindsided by these taxes only to recover their businesses stronger than ever. On the plus side, these habits you develop to tackle these taxes will help you manage your money in other aspects of your business.

Hopefully this guide gave you the tools you need to make your business run more smoothly and get you started on your own tax strategy. Taxes are your biggest expense and knowing how to address them is critical to keeping you constantly moving towards your goals. Now you have some valuable questions to ask yourself to start crafting your own tax strategy.